The Group-Theoretical Analysis of Nonlinear Optimal Control Problems with Hamiltonian Formalism

- DOI

- 10.1080/14029251.2020.1683985How to use a DOI?

- Keywords

- Nonlinear optimal control problems; theory of Lie groups; dynamic optimization; Hamiltonian formalism; Pontryagin’s maximum principle; economic growth models

- Abstract

In this study, we pay attention to novel explicit closed-form solutions of optimal control problems in economic growth models described by Hamiltonian formalism by utilizing mathematical approaches based on the theory of Lie groups. For this analysis, the Hamiltonian functions, which are used to define an optimal control problem, are considered in two different types, namely, the current and present value Hamiltonians. Furthermore, the first-order conditions (FOCs) that deal with Pontrygain maximum principle satisfying both Hamiltonian functions are considered. FOCs for optimal control in the problem are studied here to deal with the first-order coupled systems. This study mainly focuses on the analysis of these systems concerning for to the theory of symmetry groups and related analytical approaches. First, Lie point symmetries of the first-order coupled systems are derived, and then by using the relationships between symmetries and Jacobi last multiplier method, the first integrals and corresponding invariant solutions for two different economic models are investigated. Additionally, the solutions of initial-value problems based on the transversality conditions in the optimal control theory of economic growth models are analyzed.

- Copyright

- © 2020 The Authors. Published by Atlantis and Taylor & Francis

- Open Access

- This is an open access article distributed under the CC BY-NC 4.0 license (http://creativecommons.org/licenses/by-nc/4.0/).

1. Introduction

By analyzing the optimal control problems, the calculus of variations is one of the approaches constructed on the use of Lagrangian and Hamiltonian functions and the Euler-Lagrange equations [4, 9, 12, 22]. An optimal control problem is modeled with a state variable describing the state of the system at any point in time, a control variable dealing with the choice of variables and constraint function.Besides, the necessary conditions for Pontryagin’s maximum principle provide the determination of the costate variable [6, 45]. These conditions are defined via the first-order partial derivatives of the Hamiltonian function with respect to control, state, and costate variables, which are called the first-order conditions (FOCs). From the mathematical point of view, these conditions (FOCs) generate the systems of first-order ordinary differential equations (ODEs). Moreover, it can be varied with respect to the formulization of the optimal control problem. It is clear that the consideration of the current value Hamiltonian is more desirable since the maximum principle demands the differentiation of present value Hamiltonian in which the discount factor further adds complexity to the derivatives [1].

In addition to the current value Hamiltonian functions, the present value Hamiltonian functions can be considered for the analytical solutions of the optimal control problems in the study and then one can consider the first-order system of ODEs obtained via the first-order conditions in order to analyze by some novel mathematical methods, which are Lie symmetry groups, Jacobi last multiplier (JLM), and λ-symmetries and deal with the analytical solutions by considering the first integrals (or conservation laws) of the systems. The theory of Lie groups developed in the 19th century by Norwegian mathematician Sophus Lie [24] and was constructed to investigate the similarity solutions of systems of differential equations. After the studies of Lie, in the 20th century many researchers with the advancing computer technology interested in Lie theory and did important contributions to this field. In particular, [8,39] contain many references to further contributions. It is known from the Lie theory it is not possible to determine to Lie symmetries of these systems by package programs such as MathLie or GEM [5, 10] since there is no a regular procedure to determine Lie point symmetries of first-order ODEs, unlike higher-order ODEs. This is one of the difficulties to deal with symmetries of the first-order systems of ODEs. In addition, the investigation of Lie symmetries of optimal control problems can be troublesome because of the complexity of finding the solution of a corresponding overdetermined system of PDEs, called determining equations, in particular for the system of the first-order ODE.

It is known that the method of Jacobi last multiplier (JLM) and λ-symmetry have a direct relationship with Lie point symmetries. The JLM approach built up by Jacobi [19,20] for the application of the multipliers to classical mechanics problems. Moreover, he demonstrated that the JLM method could be used to determine the first integrals of second-order ODEs. The connection between Lie point symmetries and the multipliers are revealed by Sophus Lie [24]. After long years, Nucci and her workmates presented the relation of the Jacobi method with Lagrangian and multipliers [34–38]. Then the researchers have done many notable studies based on the applications of this method [13, 18, 26]. λ-symmetry approach can be considered as the other Lie point symmetry related method developed by Muriel and Romero using the definition of new prolongation formula on a λ-function [27–29, 44]. This approach includes some notable connections between the first integrals and the integrating factors of ODEs. Even though λ-symmetry was constructed for the reductions of the second-order ODEs that do not have Lie point symmetries, however, it can be said that λ-symmetry method is a quite applicable approach to obtain the reduced forms of linear or nonlinear second-order ODEs [16, 17]. The extension of λ-symmetries to PDEs, which are called μ-symmetries, are investigated in the literature [14,15,40]. Besides the theory is applied to nonlocal equations [2, 41].

In this study, we deal with some nonlinear optimal control problems arising in the theory of economics defining by an economic model. Economic modeling is at the heart of economic theory. In economics, a model is known as a theoretical construction representing economic processes by a set of variables and a set of logical and/or quantitative relationships between them [3, 42]. In addition, the model helps to isolate and sort out complicated chains of cause and effect and influence between the numerous interacting elements in an economy. The economic model is a simplified mathematical framework designed to illustrate complex processes [9]. Therefore, the most formal and abstract of the economic models are purely mathematical models. The analysis of these models is usually based on the concept of optimization under some constraints, and dynamic optimization is one of the most common applications. Dynamic optimization can be evaluated in discrete time and continuous time [1, 6]. The economic growth models in this study are formulated in the continuous time since continuous time optimization introduces a number of new mathematical issues. In continuous time, dynamic optimization has three major approaches such as dynamic programming, variation of calculus, and optimal control theory [25, 46]. Because of the complexity of most applications, the optimal control problems are most often solved by numerically in the literature. Numerical methods for solving optimal control problems back date to 1950s [6]. Over the last decades, the optimal control problems have become more difficult related to the complexity of models, so available methods have been improved. The solutions of optimal control problems have been very important for many disciplines that are financial economics, dynamic macroeconomics theory, etc. The applications of optimal control theory have been extended to growth theory by Arrow [3], Ramsey [42], Solow [45], Lucas, Uzawa and Romer [25, 43, 46] and others [1, 4, 9, 11, 12, 21, 22]. For a great majority of economic models, the integrand function contains a discount factor and in such cases, the current value Hamiltonian is more useable, which is independent of discount factor and it is more desirable in economic analysis [1, 30]. In the literature, there are some studies on optimal control problems by using the partial Hamiltonian method dealing with only the current value Hamiltonian [30–33].

In this paper, we focus on two different optimal control problems. The explicit closed-form analytical solutions based on symmetry group properties and mathematical relations related to Jacobi last multiplier and λ-symmetry methods are analyzed by considering related conditions of the models. This paper is devoted to present the applications of mathematical methods to optimal control problems to investigate not only the analytical solutions and but also the solutions of initial-value problems by organizing as follows. Section 2 consists of important properties of the mathematical methods. Section 3 includes an optimal growth model with environmental asset. Section 4 consists of the analysis of planner’s problem, which is another growth model in economics. Some considerable conclusions and discussions on the study are introduced in Section 5.

2. Preliminaries

2.1. Optimal control problems and Hamiltonian functions

Let us consider a decision problem to maximize the total profits of a firm for an interval of time t.In this problem, there are three important variable functions of time. First, q(t) is the stock of capital of a firm, c(t) is a decision function, and u = u(t,q,c) is the net profit of a firm per unit time. In order to obtain the total net profit for the terminal date T, it should be integrated for all interval of time, where the initial date is taken as t = 0, that is

In general, the optimal control problems are considered of the form

Definition 2.1.

The present value Hamiltonian is defined as

Remark 2.1.

The necessary conditions for optimal control based on the Pontryagin maximum principle for present value Hamiltonian

The conditions (2.9)–(2.11) and (2.12)–(2.14) derive optimality with all variables starting out from any given initial position. By this way, both optimal control problems and associated optimal initial values become much more simple for determining the optimality. In this study, the analysis of the optimal control problems in economic growth models is considered by taking into account both current value Hamiltonian and present value Hamiltonian functions.

2.2. The method of Jacobi last multiplier

It is known that one of the most efficient methods for the investigation of the solutions of differential equations is based on the study of Lie group of transformations. In addition, in the literature, there are some methods related to Lie symmetries such as λ-symmetry and Jacobi last multiplier, which are highly effective to obtain the reduced form of given equation in order to study the first integrals. One of them is Jacobi last multiplier method and its important relations with first integrals and multiplier for ODEs and multidimensional systems whose Lie symmetries are known [34–37].

The method of JLM enables to derive all the solutions of the partial differential equation,

Then the multiplier of this system M is indicated by the formula

In addition, it can be expressed equivalently

Actually, the existence of a solution/first integral is a result of the existence of a symmetry, Lie in [23], presented an alternative formulation in terms of symmetries. The formulation in terms of solutions/first integrals and symmetries is pointed out by Bianchi [7]. If n − 1 symmetries of system (2.16) are known

3. Optimal Growth Model with Environmental Asset

In this part, as a first economic model of the study, the problem called an optimal growth model with an environmental asset is analyzed [21]. In this problem, the asset is evaluated as natural capital or environmental quality and it is valued both as a source of consumption of environmental services and as a stock of amenities. This model is formulated as an optimal control problem in which the social planner seeks to maximize the integral

Definition 3.1 (Tranversality condition).

This condition is an optimally condition often used to characterize the optimal paths (plans, programs, trajectories, etc.) of economic models. The transversality condition is essential in infinite-dimensional problems since it makes sure that there are no beneficial simultaneous changes in an infinite number of choice variables [1].

3.1. First integrals and analytical solutions for current value Hamiltonian

To obtain a solution of the problem (3.1) and (3.2), first we consider the current value Hamiltonian for the model (3.1) written via (2.8) in the form

To evaluate the solution of the optimal control problem, the appropriate initial conditions should be considered for state, control, and costate variables in the formulation of the problem. For this model, the related initial conditions are

By considering the system of coupled ODEs with the elimination of control variable c(t) from the equations (3.4)–(3.6), the related first-order system of ODEs

Proposition 3.1.

The system of first-order coupled differential equations (3.10) – (3.11) possesses four-dimensional Lie algebra L4.

Proof.

It can be shown that the direct integration of the determining equations in terms of t, p, and s variables gives the following four-dimensional Lie algebra L4

Based on the JLM method by utilizing the equations (2.20)–(2.21) the multipliers of the system (3.10) can be determined as the following form

Analytical solutions. By using the ratio of Jacobi last multipliers in (3.13), the first integrals of the system can be derived and via these first integrals closed-form solutions can be obtained. For instance, the first integral

Remark 3.1.

One can observe that the first integral does not involve the time derivatives of the variables, that is, it is an algebraic equations as expected.

The use of transversality condition. The next step is to consider the initial conditions and transversality condition for the solutions in (3.15)–(3.17) to analyze an initial-value problem. If the transversality condition (3.9) is written in the form

The solution of initial-value-problem. By using the initial conditions c(0)= c0 and s(0)= s0, the solution of the initial-value problem satisfying also the transversality condition becomes

One can observe that the growth rates given by (3.20) and (3.21) are equal to each other and this constant rate is meaningful for the economics sense. Another growth rate related to the costate variable p increases at a constant rate by the factor

3.2. First integrals and analytical solutions for present value Hamiltonian

As an alternative approach to the solution of the optimal control problem we consider the corresponding present value Hamiltonian for the problem provided by (3.1) and (3.2) pf the form

By the same manner used in the previous section, the first-order system of ODEs related to the present value Hamiltonian can be written by eliminating the control variable

Proposition 3.2.

The system of first-order coupled differential equations (3.27)–(3.28) possesses six-dimensional Lie algebra L6.

Proof.

The standard but some troublesome calculations for the related determining equations yield the Lie point symmetries of the system (3.27)–(3.28) as a six-dimensional Lie algebra L6 such that

Remark 3.2.

For the optimal growth model with environmental asset, one can point out again the difference between the current Hamiltonian and the present Hamiltonian functions in terms of Lie point symmetries. For the case of current Hamiltonian function, the system has four-dimensional Lie algebra L4, in the case of present value Hamiltonian the system has six-dimensional Lie algebra L6. It can be seen that this property is different from the case of the first control problem.

Based on the JLM method is given in Section 2.2, via the Lie symmetries (3.29) the multipliers of the system (3.27) can be obtained as the following form

The first integral of the system can be derived by the JLM method and in order to determine analytical solution for the system (3.24)–(3.26), we can use related first integral

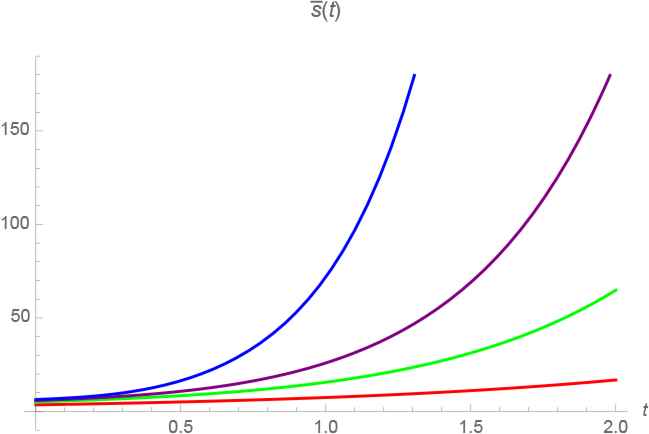

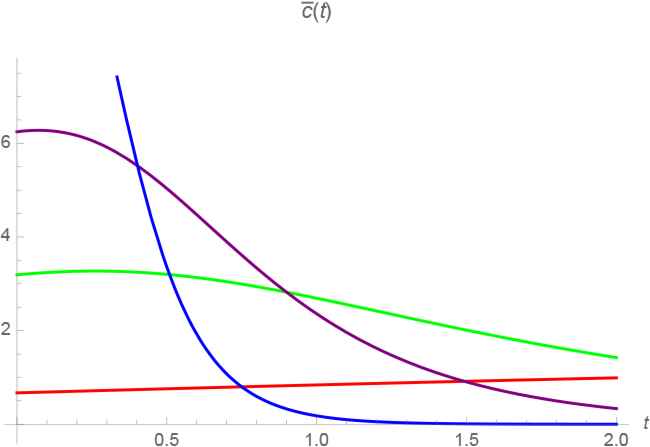

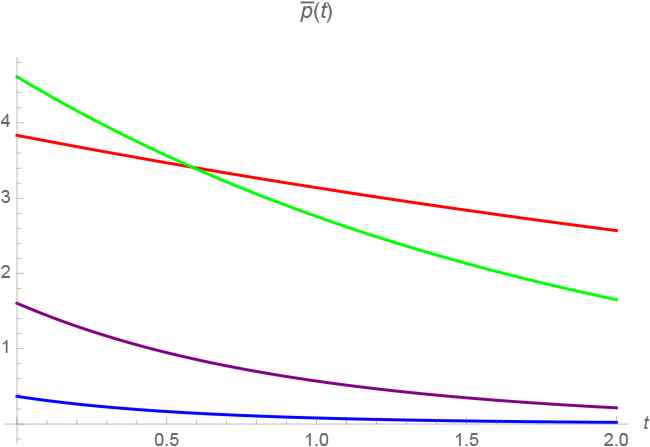

Graphical representations of the solutions. In order to explain the physical interpretation of solution surfaces in the analytical solutions, the two dimensional plots are shown below. The time variation of variables for the stock environmental asset function s(t), the consumption function c(t), and the costate variable p(t) are represented.

Figures 1–2–3 show the state, control and costate variable versus the time t, for the parametric choices φ, σ, ρ, m such that 0.9, 1.5, 2 and 3 with the same value integration constants c1 and c2.

The graph of state-simulation representing the Eq. (3.33) The graph of control variable representing the Eq. (3.34) The graph of costate variable in the Eq. (3.35)

The use of transversality condition. The transversality condition for (3.33)–(3.35) reads

The solution of initial-value-problem. Thus, the associated solution of the initial-value problem satisfying the transversality condition can be written as

As a result, the growth rates for the control problem (3.1) and (3.1) defined by all of the economic variables are introduced by the following ratios

3.3. Lagrangian approach

In addition, the equivalent second-order differential equation in terms of s(t) stock environmental asset variable can be constructed by implementing Euler-Lagrange differential operator to the Lagrangian according to the relation

Proposition 3.3.

The second-order nonlinear ordinary differential equation (3.41) possesses eight-dimensional Lie algebra L8.

Proof.

The differential equation (3.41) yields the eight-dimensional symmetries L8 as below

Remark 3.3.

If the second order ODE in the form

Remark 3.4.

If it is known that the pair (∂x,λ) is a λ-symmetry of a given second order ODE, then first integral and integrating factor can be evaluated using the following procedure [28]:

- 1.

Derive a first integral ω(t,x,

- 2.

Determine A(ω) and express A(ω) in terms of (t,ω) as A(ω)= F(t,ω).

- 3.

Find a first integral G of ∂t + F(t,ω)∂ω.

- 4.

Evaluate the final form of first integral as

Here, by using these symmetries, the first integrals of the equation can be evaluated with respect to the Jacobi and λ-symmetry approaches as two different cases.

Case I. In order to consider the λ-symmetry method, first, it can be shown that, for example, the symmetry X3 leads to ξ= 0 and η= e(1+φ)mts−φ. Then via Remark 3.3, the characteristic function and the infinitesimal vector field are written by

Hence, the λ-symmetry is derived by in the form

If the steps, which are expressed in Remark 3.4, are followed for λ-symmetry (3.46) and then the integration factor and first integral

Case II. The possible Jacobi Last Multipliers are the reciprocals of the nonzero determinants of the possible matrices of (2.21). JLMij is indicated a multiplier, where the i and j refer to the symmetries used in the determinants. For example, by using the two symmetries, X1 and X2, one can write the corresponding determinant

4. Planner’s Problem

As the last optimal control problem of the current study to analyze, we take into consideration the planner’s problem that defines a growth model in economics [22]. In the literature, this problem is analyzed numerically by using Runge-Kutta scheme based on exponential Lawson integration for nearly Hamiltonian systems [11]. In fact, this problem states that an economy produces a consumption good whose output is u(t), and the main purpose is to determine u(t) >0 that maximizes the integral

Similarly, if we focus on the present value Hamiltonian function including the discount factor of the form

By the use of the relationship between Lagrangian and Hamiltonian (present value Hamiltonian), the Lagrangian function related to Hamiltonian function (4.8) of the differential equation (4.12)

Proposition 4.1.

The second-order nonlinear ordinary differential equation (4.12) has two-dimensional Lie algebra L2.

Proof.

It can be easily checked that the equation (4.12) possesses two-dimensional Lie symmetries from solutions of the corresponding determining equations, namely,

Based on the procedure given by Remark 3.3 and Remark 3.4, the generator X2 yields

Analytical solutions. The first integral I1 gives the solution for the stock of pollution variable

Remark 4.1.

There may exist JLMs not derived from symmetries via (2.21). Therefore, although equation (4.12) has only two Lie point symmetries, the JLM method could still be applicable to obtain first integrals of the equation.

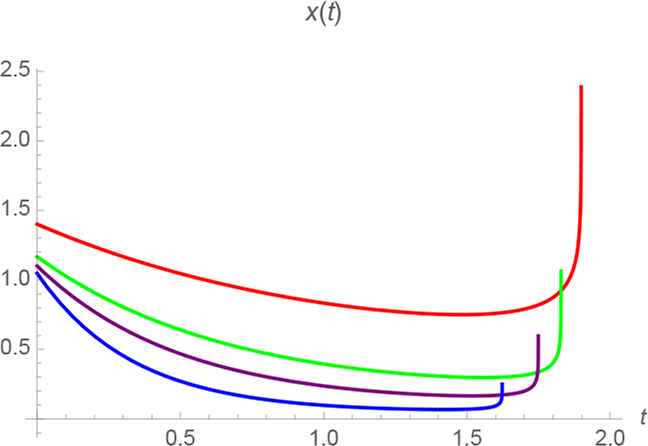

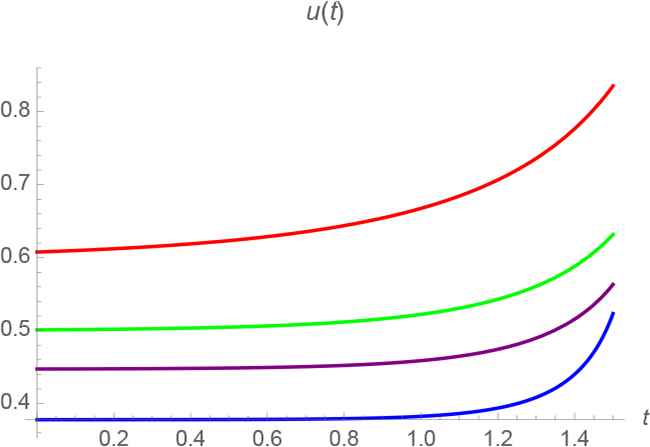

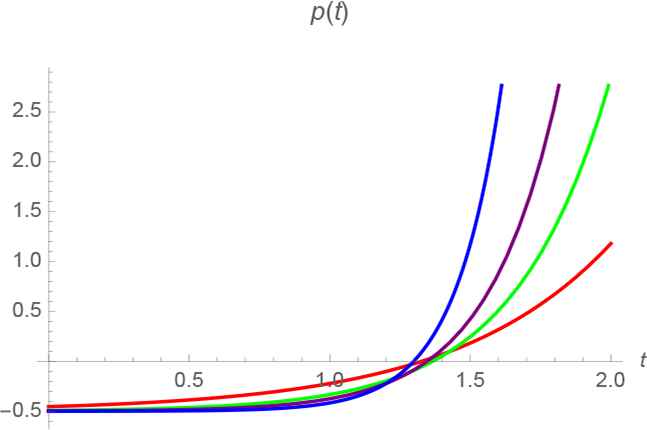

Graphical representations of the solutions. Similarly, in order to explain the physical interpretation of solution surfaces in the analytical solutions, the two dimensional plots are shown below. The time variation of variables for the consumption good output function u(t), stock of pollution x(t), and the costate variable p(t) are represented.

Figures 4–5–6 represent the state, control and costate variables of planner’s problem (4.1) versus the time t, with the values of the parameters λ, b, ρand m are chosen by 0.9, 1.5, 2 and 3 for the same value integration constants c1 and c2.

The graph of state-simulation representing the Eq. (4.18) The graph of control variable of the Eq. (4.19) The graph of p − t of the Eq. (4.20)

The use of transversality condition. On the other hand, the transversality condition (4.3) by considering the equations (4.18)–(4.20) requires that ρ >0. Thus, the growth rates are

Remark 4.2.

The relations

Proposition 4.2.

It is possible to obtain the similar results given by (4.18)–(4.19) for the model (4.1) and (4.2) by using the partial Hamiltonian method.

Proof.

The partial Hamiltonian method can also be applied to the maximization problem given in (4.1) and (4.2) by the current value Hamiltonian (4.4). We here only represent the results based on this method for the problem (4.1) and (4.2). The corresponding infinitesimal functions and the gauge function B [32] are found as

On the other hand, it can be checked that if the FOCs are used to determine the solution of stock of pollution x(t) then the necessary calculations confirm that the same solution is found with the solution given in (4.18).

Remark 4.3.

For all first integrals I and Ī obtained in three different economic models, it can be verified that the relations DI = 0 and DĪ = 0 yield the corresponding original differential equations.

5. Conclusions and Remarks

In this study, we analyze for the first time in the literature the analytical solutions of some economical models, which are entitled the optimal control model with environmental asset and the planner’s problem, by using different mathematical approaches having notable mathematical connections based on the symmetry group theory. In the literature, the optimal control problems in economic growth theory are generally investigated by numerical methods because of complexity of the formulizations of the models. The methods used here focus to determine analytical solutions of the optimal control problems in the theory of economics and it can be seen as one of the remarkable contributions in this study. Besides, another considerable property of the study is based on the fact that the first-order conditions (FOCs) are considered not only for the current value Hamiltonian but also for the present value Hamiltonian. The first-order conditions are called Hamiltonian equations for the case of present value Hamiltonians.

The novel and nontrivial analytical solutions for the present value Hamiltonians are investigated. Additionally, the initial-value problems are studied for the cases of optimal control model with environmental asset and the planner’s problems. After obtaining the analytical solutions, the corresponding initial conditions are applied and the solution for the related initial-value problem is determined. In addition to the initial-values related problems, the transversality conditions, which are optimal conditions often used to characterize the optimal paths of economic models, are also considered for the solution of the models. The growth rates for the control problem defined by all economic variables are introduced by the ratios of the variables and their time derivatives.

As one of the mathematical approaches, the Jacobi last multiplier method connected to the Lie symmetry groups is also applied for investigating new first integrals (conservation forms) for the system of first-order differential equations. It is shown that any ratio of two different multipliers M

For the optimal control model with environmental asset, we show that system of first-order differential equations associated with the current value Hamiltonian and the present value Hamiltonian have different forms and this property is an important reason to deal with two different Hamiltonian functions based on the analytical solutions for the optimal control problems. We also prove a remarkable distinction between the current Hamiltonian and the present Hamiltonian functions with respect to their Lie point symmetries. In the case of the optimal growth model with environmental asset we have four-dimensional Lie algebra L4 for the current value Hamiltonian and five-dimensional Lie algebra L6 for the present vale Hamiltonian. This can be seen as an important property for the analysis of the optimal control problems.

For the analysis of the first-order system of ordinary differential equations, we indicate that the first integrals are algebraic equations of the dependent variables since the system has only first-order derivatives. However, in the case of single second-order ordinary differential equations, the first integrals involve the first-order time derivatives of the unknown functions as can be expected. For the optimal growth model with environmental asset, we obtain not only the analytical solutions but also the solutions of the initial-value problem based on the initial conditions and the transversality condition. For the planner’s problem, we also show that the relations

In this study, we also emphasize the fact that the applied procedures such as JLM and λ-symmetries and connection with Lie symmetries can represent new perspectives for the optimal control problems in economic growth models. For example, the method of Jacobi can provide the first integrals for a given equation since any ratio of two multipliers equal to a first integral and then the growth rates of optimal growth model with environmental asset can be determined for the results of current and present value Hamiltonians. Additionally, the analytical solutions for the different value of the parameters are represented by the solution graphs and some mathematical economic comments belong to them are explained. In addition, to compare the results for the case of the planner’s optimal control model, we prove that the application of the mathematical methods considered in the study and the partial Hamiltonian method yield the same results.

In addition, from another mathematical point of view, it is known that it is not possible to apply the phase diagram approach as the usual method since the equilibria can not be defined well for analysis of the optimal control problems including the independent time exponential term that the present value Hamiltonian function involves. In this study, however, we represent that the analysis of optimal control problems in economic growth models by the theory of Lie groups involving not only the current value Hamiltonian function but also present value Hamiltonian function can be carried out analytically and effectively.

References

Cite this article

TY - JOUR AU - Gülden Gün Polat AU - Teoman Özer PY - 2019 DA - 2019/10/25 TI - The Group-Theoretical Analysis of Nonlinear Optimal Control Problems with Hamiltonian Formalism JO - Journal of Nonlinear Mathematical Physics SP - 106 EP - 129 VL - 27 IS - 1 SN - 1776-0852 UR - https://doi.org/10.1080/14029251.2020.1683985 DO - 10.1080/14029251.2020.1683985 ID - Polat2019 ER -