On Partially Linear Single-Index Models with Missing Response and Error-in-Variable Predictors

- DOI

- 10.2991/jsta.d.190306.006How to use a DOI?

- Abstract

In this paper, we consider a partially linear single-index model when missing responses and nonlinear regressors with measurement error are taken into account. Utilizing data imputation for missing values and regression calibration for error-prone regressors, we not only estimate the parameters in the linear part as well as the single-index part, but also estimate the nonparametric link function by local linear fit. Under normalization, all the proposed estimators for the regression coefficients and the link function are proven to be asymptotically normal, and some illustrative simulations are provided to justify our methods.

- Copyright

- © 2019 The Authors. Published by Atlantis Press SARL.

- Open Access

- This is an open access article distributed under the CC BY-NC 4.0 license (http://creativecommons.org/licenses/by-nc/4.0/).

1. INTRODUCTION

To avoid the so called “curse of dimensionality” in the nonparametric or semiparametric regression analysis, partially linear single-index models (PLSIM) emerged as an effective device for dimension reduction; see, for example, Härdle and Stoker [1], Powell et al. [2], Newey and Stoker [3], Ichimura [4], Carroll et al. [5], Xia and Härdle [6], Lu and Cheng [7], and many others. Served as an effective way of modelling a nonlinear relationship between several covariates and their response, PLSIM, however, might obtain biased estimations when the covariates and/or their response are not complete.

When one collects data (e.g., survival data), due to many practical problems, he may obtain an incomplete data set which, to such an extent, may lead to a biased estimation. Therefore, the augmentation of the missing data becomes more and more important in the data demanded world. In general, missing data might emerge in both of the responses and covariates, while in this paper we will mainly focus on the case when solely the response is missing. According to the nature of missing data, Little and Rubin [8] firstly classified the types of missingness into three categories—missing completely at random (MCAR), missing at random (MAR), and missing not at random (MNAR). In the present paper, we will consider the MAR mechanism (see, e.g., Wang et al. [9], Yun et al. [10]) which kicks in when the probability that a response is missing dose not depend on the unobserved measurements. A very important type of missingness is censoring; in particular, for the censoring case in PLSIM, Lu and Cheng [7] adopted a Kaplan–Meier-like transformation to overcome the biasedness of the estimation of the coefficients and link function. Besides, Cheng et al. [11] considers a more difficult problem concerning the estimation of the parameters and nonparametric function for a PLSIM with censored response and covariates having measurement error. However, for general missingness of the responses in PLSIM, there’s not a paper studying on it.

Another important issue concerning incomplete data is about measurement error. Measurement error models have been largely studied in the literature, for example, Fuller [12], Carroll [13], Carroll and Stefanski [14], Carroll and Li [15], Lue [16], and Fan and Troung [17], among others. It was indicated by Carroll et al. [18] that, there are three effects caused by measurement errors: first, it causes bias in parameter estimation for statistical models; second, it leads to a loss of power, sometimes profound, for detecting interesting relationship among variables; finally, it makes the features of the data, making graphical model analysis difficult. Especially, the effects of biasedness of the parameters become severer especially when the relationship between the covariates and responses appear to be nonlinear.

In this paper, we consider the following PLSIM

Among the wide variety of procedures to handle missing data, data imputation is an important step. By imputing a plausible value for each missing datum, under mild conditions, the problem can be dealt with as if they were complete. Different categories of imputations can be found in Schulte Nordholt [19]. The first classification, roughly speaking, comprises the deterministic as well as the stochastic imputations [20]. The second classification is a distinction between naive and principled approaches. The naive imputations, mainly based on analyzing complete cases (listwise or pairwise), are a quick option. For example, the imputation of an unconditional mean is a naive approach. It might lead to a biased estimate even if the data are randomly missing. Little and Rubin ([8] Chapter 3) indicated that the obvious corrections of this biasedness will obtain the same estimates as found with available case procedures. The principled approaches adopt models for both the observed and missing data on which the imputations are based.

Besides, there is a distinction between imputations according to “explicit” and “implicit” models [21, 22]. Examples can be referred to the hot-deck procedures [23], in which missing values are imputed with donor cases from the set of completely observed cases. There are still many other imputation methods, for example, linear regression imputation [24], multiple imputation [20, 25], nonparametric kernel regression imputation[26, 27]), nearest neighbor imputation [28], ratio imputation [29], regression calibration [30], and semiparametric regression imputation [9], and so on. Wang and Sun [31] adopted semiparametric imputation, semiparametric regression surrogate and inverse marginal probability weighted (IMPW) approaches, separately, to estimate

2. PROCEDURES OF ESTIMATIONS

2.1. Carroll and Li’s Transformation

As mentioned in the introduction, how to calibrate the contaminated regressors to be unbiased is a very important issue. The Carroll and Li’s [15] transformation, as stated in the following, is nothing more than a simple linear prediction of

Suppose on the other hand that, we have a replicated data rather than a validation sample. As in Carroll and Li [15] and Lue [16], we consider an important special case when

If

With this choice of

2.2. Estimations of PLSIM with Missing Response and Error-Prone Predictors

Consider the PLSIM model defined by Eq. (1). In this section, we assume that we are given a data set with partially missing response and error-prone regressors in the nonlinear single-index term. In order to remedy the biasedness of estimations caused by missing and measurement error, we propose a modified quasi log-likelihood estimation procedure via an iterative minimization algorithm.

Let

In the case when the data consists of MAR response variables and error-prone regressors, some auxiliary treatment of the data set is necessary. A difficulty common to single-index model is that, minimizing Eq. (6) involves the estimation of the nonparametric function

We denote the transformed

In order to claim that, when we replace

Now we return to the case as

Our estimation algorithm consists of the following steps:

Step 1: Treat the synthetic data

Step 2: Find

Step 3: Update

with respect toStep 4: Iterate Steps 2 and 3 until convergence is achieved.

3. ASYMPTOTIC THEOREMS FOR THE ESTIMATORS

In this section, we will establish the asymptotic normality of the estimators of the parameters emerging in the PLSIM model. Condition A is given to ensure the asymptotic properties of the estimators to hold.

Condition A.

The kernel

The random vectors

The marginal density

The random vector

The functions

For a given

Let

both

Theorem 1.

Under Condition A and the following conditions on the bandwidth:

Theorem 2.

Under the same conditions as given in Theorem 1, the estimator

It is interesting to note that

By the root-n consistency of

Theorem 3.

Let

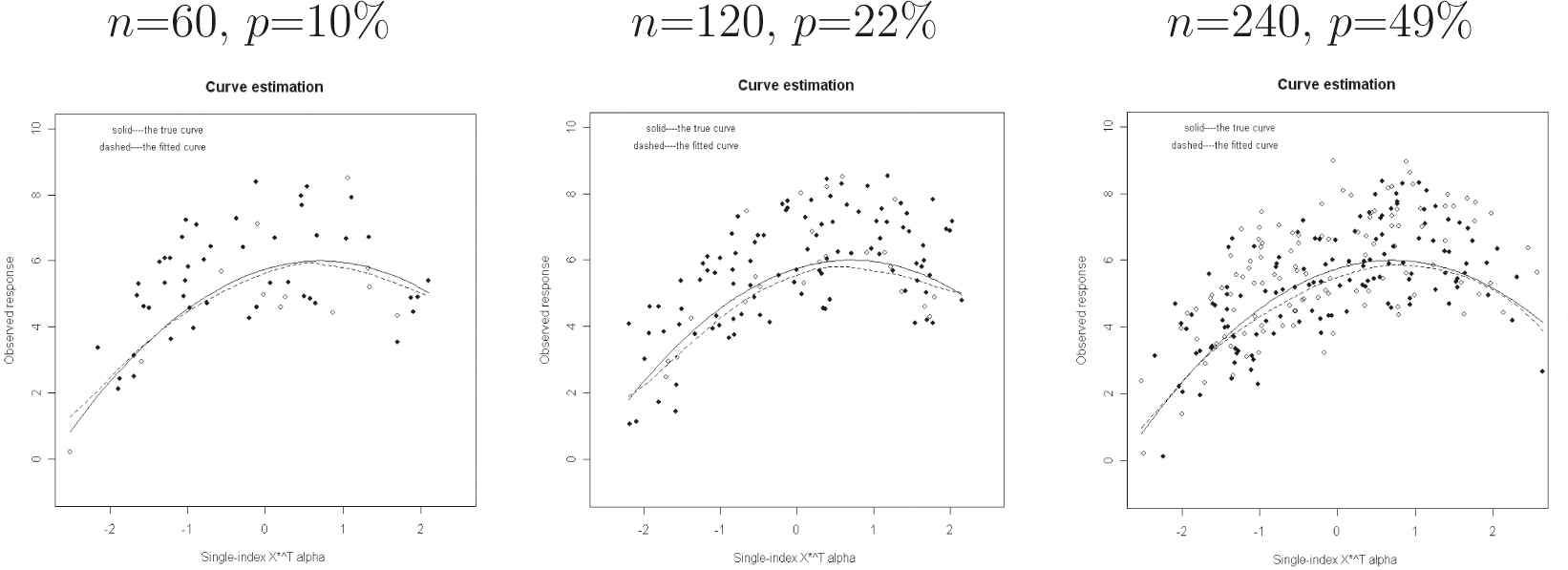

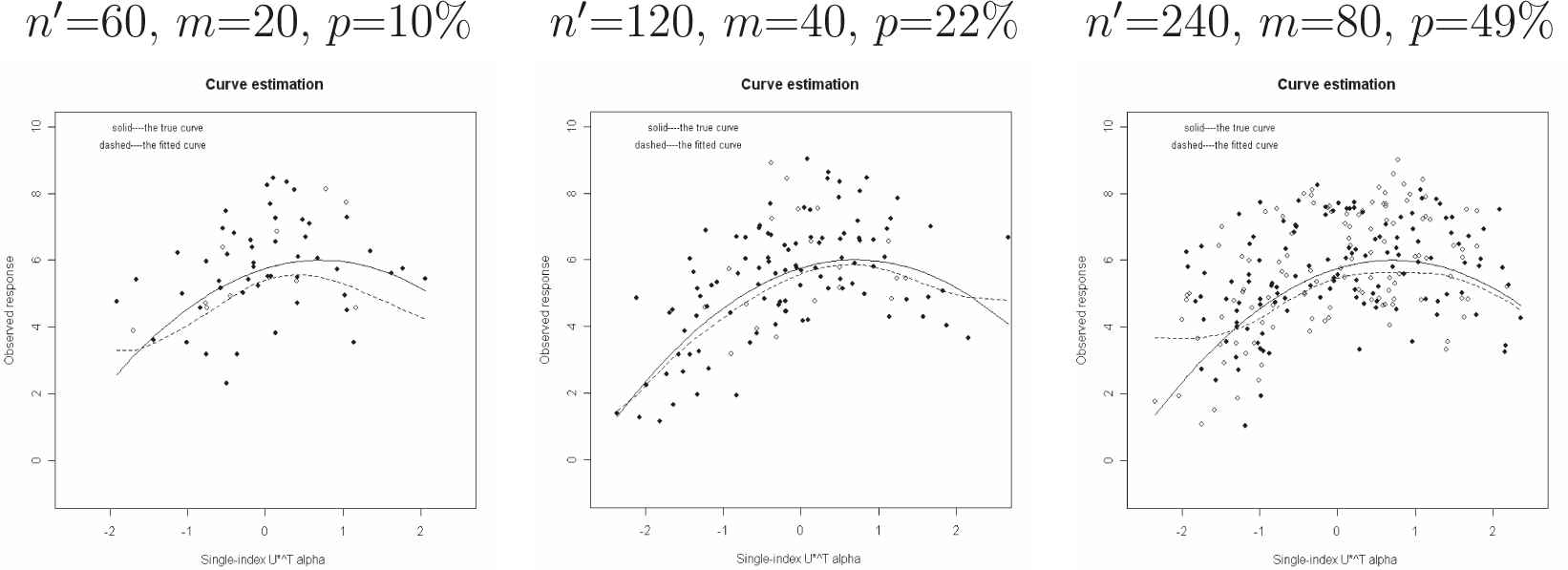

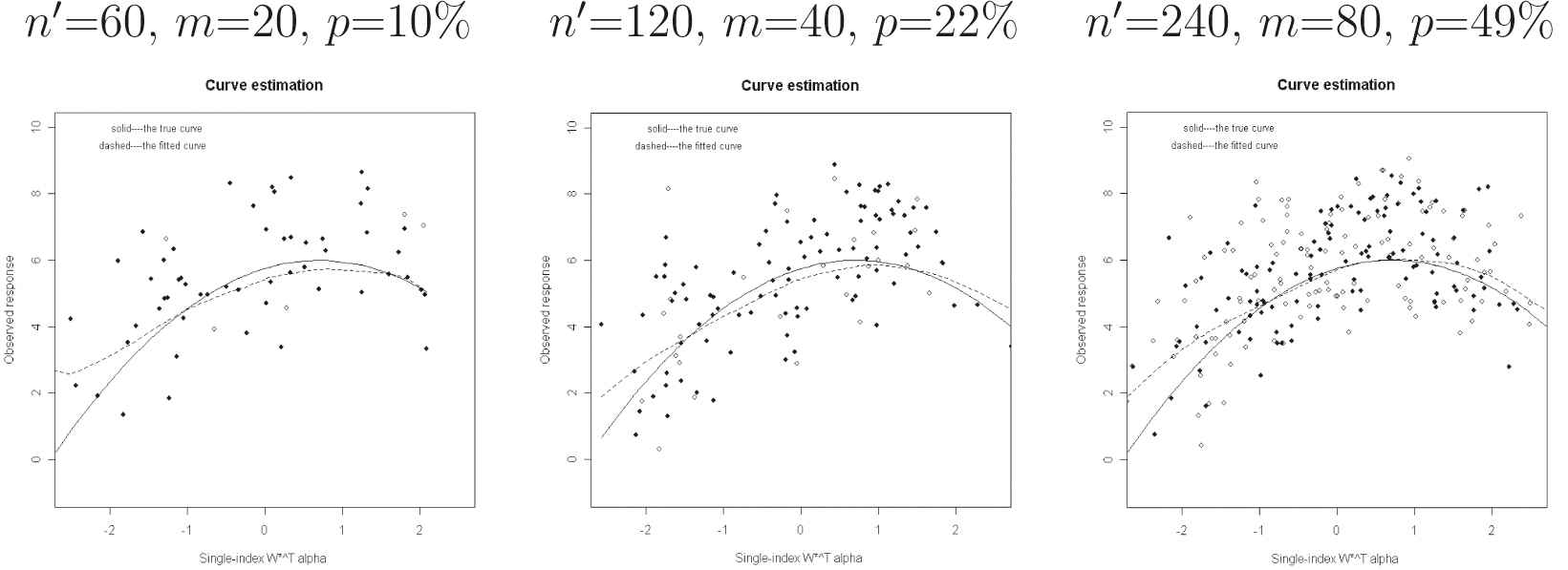

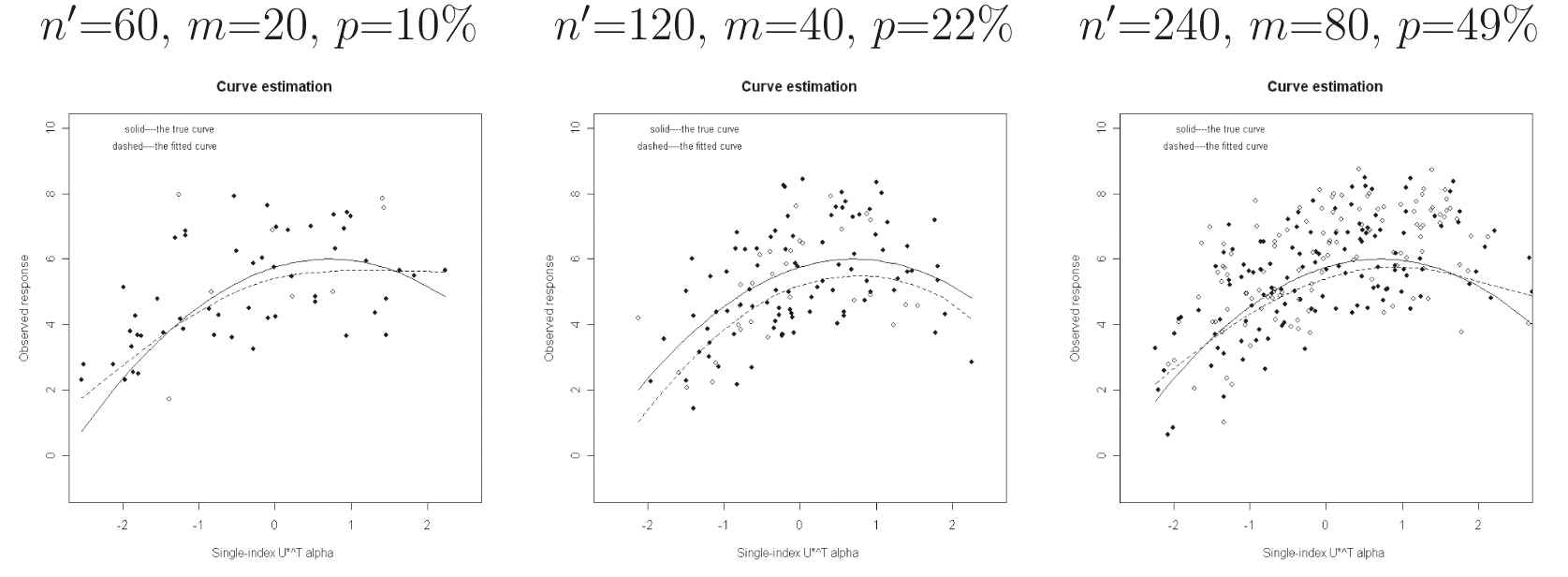

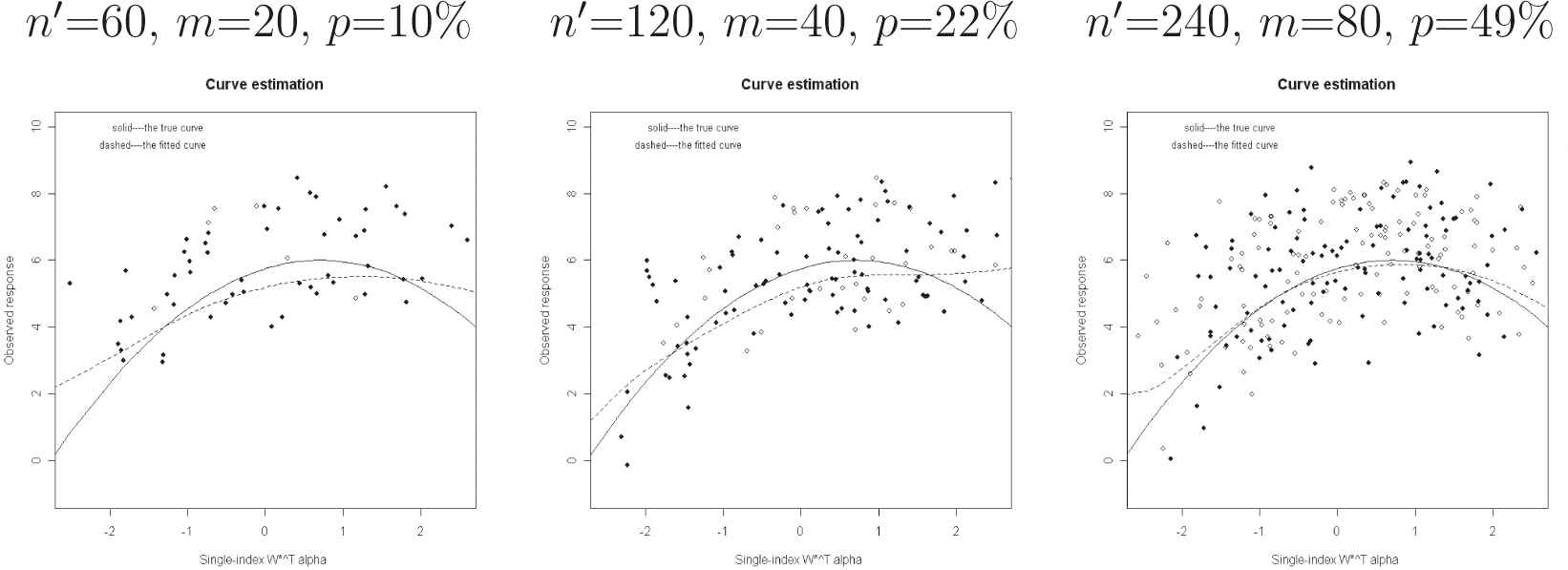

4. SIMULATION

Example

In this example, we conduct some Monte Carlo simulations to estimate the regression coefficients for an partially single-index model with incomplete data, and

Case 1:

Case 2:

Case 3:

By conducting Monte Carlo simulations, the mean response rates of the above three cases are

In Table A.1 (resp. Table A.4), we report the results of

From Tables A.1 and A.4, all the proposed estimates of

APPENDIX I

Proof of Theorem 1. and 2.

The proof of Theorem 2 is just a part of arguments used in the proof of Theorem 1, therefore we omit it. Here, we give a detailed proof of Theorem 1 only.

Denote

The proof consists of two steps. The first step is to obtain an expansion for

We will show that

Denote the

Then, we will obtain the following representation:

Proof of (A.2).

Let

Solving the above equation for

Let

Since

Substituting the kernel terms in the linearized Eq. (A.4) by their asymptotic counterparts, we obtain Eq. (A.2).

Proof of (A.3).

By a Taylor expansion, we have

With

Let

By Taylor expansion, we obtain

Since

By Eq. (A.8), we get

Plugging this into Eq. (A.9) gives

This leads to

Note that by using matrix notation,

Then from Eq. (A.2) and the definition of

It is easy to see that the sixth term is Eq. (A.10) is

From

Multiplying both sides by

Section I.1. Proofs of (A.5) and (A.7)

Proof of (A.5).

Let

Equation (A.12) will be used in the proof of Eq. (A.6). First, we assume that Eq. (A.13) holds and we prove Eq. (A.12). Let

Now we prove Eq. (A.13). Let

We consider

To finish the proof, it suffices to show

We prove Eq. (A.16) but Eq. (A.17), since Eq. (A.17) is very easy to prove. We consider a more general case where

When

Suppose that

By Condition A(ii), there exists some constants

Therefore,

Similarly,

Taking

Since

This implies

Combining Eqs. (A.20) and (A.21) proves Eq. (A.18).

Now we prove Eq. (A.19). By Conditions A,

Proof of (A.7).

Since

Section I.2. Proof of (A.6)

Proof of (A.6).

Since

The proof of Eq. (A.23) is similar to that of Eq. (A.12), we omit it. Now we prove Eq. (A.24). Note that

By decomposition, it suffices to show

We shall apply the similar techniques used in the proof of Eq. (A.16) to prove the preceding three equalities. By Conditions A(ii) and (iv),

Section I.3. Proof of (A.11)

Proof of Eq. (A.11).

To prove Eq. (A.11) is equivalent to prove the following equality:

Noting that

It implies that

Now we return to the proof of Theorem 1. In Eq. (A.3),

Therefore, by Eq. (A.31), we have shown that

APPENDIX II

| MEAN | SD | RMSE | MED | MEAN | SD | RMSE | MED | ||

|---|---|---|---|---|---|---|---|---|---|

| p = 10%, n = 60 | |||||||||

| 0.707 | 0.710 | 0.061 | 0.061 | 0.707 | −1 | −0.998 | 0.148 | 0.147 | −0.999 |

| 0.707 | 0.699 | 0.064 | 0.065 | 0.707 | 2 | 2.003 | 0.149 | 0.148 | 2.007 |

| p = 22%, n = 120 | |||||||||

| 0.707 | 0.709 | 0.044 | 0.044 | 0.707 | −1 | −0.995 | 0.107 | 0.107 | −0.994 |

| 0.707 | 0.703 | 0.045 | 0.045 | 0.707 | 2 | 2.005 | 0.114 | 0.114 | 2.005 |

| p = 49%, n = 240 | |||||||||

| 0.707 | 0.704 | 0.038 | 0.038 | 0.707 | −1 | −1.002 | 0.096 | 0.096 | −0.998 |

| 0.707 | 0.708 | 0.037 | 0.037 | 0.707 | 2 | 2.006 | 0.095 | 0.095 | 2.003 |

MED, median; SD, standard derivation ; RMSE, root-mean-square error.

Descriptive statistics of

| MEAN | SD | RMSE | MED | MEAN | SD | RMSE | MED | ||

|---|---|---|---|---|---|---|---|---|---|

| p = 10%, |

|||||||||

| 0.707 | 0.686 | 0.165 | 0.166 | 0.707 | −1 | −0.992 | 0.202 | 0.202 | −1.009 |

| 0.707 | 0.682 | 0.192 | 0.193 | 0.707 | 2 | 2.011 | 0.194 | 0.194 | 2.011 |

| p = 22%, |

|||||||||

| 0.707 | 0.673 | 0.127 | 0.131 | 0.707 | −1 | −0.995 | 0.152 | 0.152 | −0.989 |

| 0.707 | 0.718 | 0.122 | 0.122 | 0.707 | 2 | 2.007 | 0.149 | 0.149 | 2.014 |

| p = 49%, |

|||||||||

| 0.707 | 0.665 | 0.105 | 0.113 | 0.695 | −1 | −1.005 | 0.137 | 0.136 | −1.001 |

| 0.707 | 0.733 | 0.095 | 0.098 | 0.719 | 2 | 1.993 | 0.127 | 0.127 | 1.993 |

MED, median; SD, standard derivation ; RMSE, root-mean-square error.

Descriptive statistics of

| MEAN | SD | RMSE | MED | MEAN | SD | RMSE | MED | ||

|---|---|---|---|---|---|---|---|---|---|

| p = 10%, |

|||||||||

| 0.707 | 0.741 | 0.105 | 0.110 | 0.715 | −1 | −1.000 | 0.206 | 0.205 | −1.003 |

| 0.707 | 0.651 | 0.129 | 0.140 | 0.699 | 2 | 1.973 | 0.203 | 0.204 | 1.964 |

| p = 22%, |

|||||||||

| 0.707 | 0.747 | 0.080 | 0.089 | 0.740 | −1 | −0.977 | 0.138 | 0.140 | −0.981 |

| 0.707 | 0.653 | 0.097 | 0.111 | 0.673 | 2 | 1.995 | 0.150 | 0.150 | 1.987 |

| p = 49%, |

|||||||||

| 0.707 | 0.752 | 0.065 | 0.079 | 0.748 | −1 | −1.017 | 0.127 | 0.128 | −1.014 |

| 0.707 | 0.651 | 0.077 | 0.095 | 0.663 | 2 | 1.984 | 0.127 | 0.128 | 1.985 |

MED, median; SD, standard derivation ; RMSE, root-mean-square error.

Descriptive statistics of

| MEAN | SD | RMSE | MED | MEAN | SD | RMSE | MED | ||

|---|---|---|---|---|---|---|---|---|---|

| p = 10%, n = 60 | |||||||||

| 0.707 | 0.709 | 0.046 | 0.046 | 0.707 | −1 | −1.002 | 0.144 | 0.144 | −1.004 |

| 0.707 | 0.702 | 0.049 | 0.049 | 0.707 | 2 | 1.992 | 0.151 | 0.151 | 1.985 |

| p = 22%, n = 120 | |||||||||

| 0.707 | 0.710 | 0.040 | 0.040 | 0.707 | −1 | −0.989 | 0.108 | 0.108 | −0.992 |

| 0.707 | 0.701 | 0.042 | 0.042 | 0.707 | 2 | 2.000 | 0.102 | 0.102 | 1.996 |

| p = 49%, n = 240 | |||||||||

| 0.707 | 0.710 | 0.038 | 0.039 | 0.707 | −1 | −0.994 | 0.097 | 0.097 | −0.988 |

| 0.707 | 0.702 | 0.041 | 0.041 | 0.707 | 2 | 2.004 | 0.092 | 0.092 | 2.005 |

MED, median; SD, standard derivation ; RMSE, root-mean-square error.

Descriptive statistics of

| MEAN | SD | RMSE | MED | MEAN | SD | RMSE | MED | ||

|---|---|---|---|---|---|---|---|---|---|

| p = 10%, |

|||||||||

| 0.707 | 0.696 | 0.136 | 0.136 | 0.707 | −1 | −1.005 | 0.230 | 0.230 | −0.985 |

| 0.707 | 0.689 | 0.151 | 0.151 | 0.707 | 2 | 2.002 | 0.183 | 0.183 | 2.003 |

| p = 22%, |

|||||||||

| 0.707 | 0.672 | 0.113 | 0.118 | 0.707 | −1 | −1.008 | 0.168 | 0.168 | −1.001 |

| 0.707 | 0.724 | 0.109 | 0.110 | 0.707 | 2 | 1.999 | 0.154 | 0.154 | 2.002 |

| p = 49%, |

|||||||||

| 0.707 | 0.675 | 0.105 | 0.109 | 0.707 | −1 | −1.014 | 0.129 | 0.130 | −1.019 |

| 0.707 | 0.724 | 0.102 | 0.103 | 0.707 | 2 | 1.988 | 0.133 | 0.133 | 1.995 |

MED, median; SD, standard derivation ; RMSE, root-mean-square error.

Descriptive statistics of

| MEAN | SD | RMSE | MED | MEAN | SD | RMSE | MED | ||

|---|---|---|---|---|---|---|---|---|---|

| p = 10%, |

|||||||||

| 0.707 | 0.748 | 0.095 | 0.104 | 0.729 | −1 | −0.977 | 0.195 | 0.196 | −0.965 |

| 0.707 | 0.645 | 0.125 | 0.140 | 0.684 | 2 | 2.021 | 0.210 | 0.210 | 2.021 |

| p = 22%, |

|||||||||

| 0.707 | 0.751 | 0.070 | 0.083 | 0.738 | −1 | −1.001 | 0.147 | 0.146 | −0.998 |

| 0.707 | 0.651 | 0.087 | 0.103 | 0.674 | 2 | 2.008 | 0.161 | 0.161 | 2.011 |

| p = 49%, |

|||||||||

| 0.707 | 0.754 | 0.073 | 0.087 | 0.750 | −1 | −1.013 | 0.136 | 0.137 | −1.016 |

| 0.707 | 0.647 | 0.087 | 0.106 | 0.661 | 2 | 1.984 | 0.134 | 0.135 | 1.996 |

MED, median; SD, standard derivation ; RMSE, root-mean-square error.

Descriptive statistics of

Simulated curves of

Simulated curves of

Simulated curves of

Simulated curves of

Simulated curves of

Simulated curves of

REFERENCES

Cite this article

TY - JOUR AU - Tsung-Lin Cheng AU - Yin-Ying Lin AU - Xuewen Lu AU - Radhey Singh PY - 2019 DA - 2019/04/22 TI - On Partially Linear Single-Index Models with Missing Response and Error-in-Variable Predictors JO - Journal of Statistical Theory and Applications SP - 46 EP - 64 VL - 18 IS - 1 SN - 2214-1766 UR - https://doi.org/10.2991/jsta.d.190306.006 DO - 10.2991/jsta.d.190306.006 ID - Cheng2019 ER -